Beyond ETFs, who else is redefining the institutional bids landscape in the crypto marketplace for 2026

Why Does the Market Always Focus on ETFs First

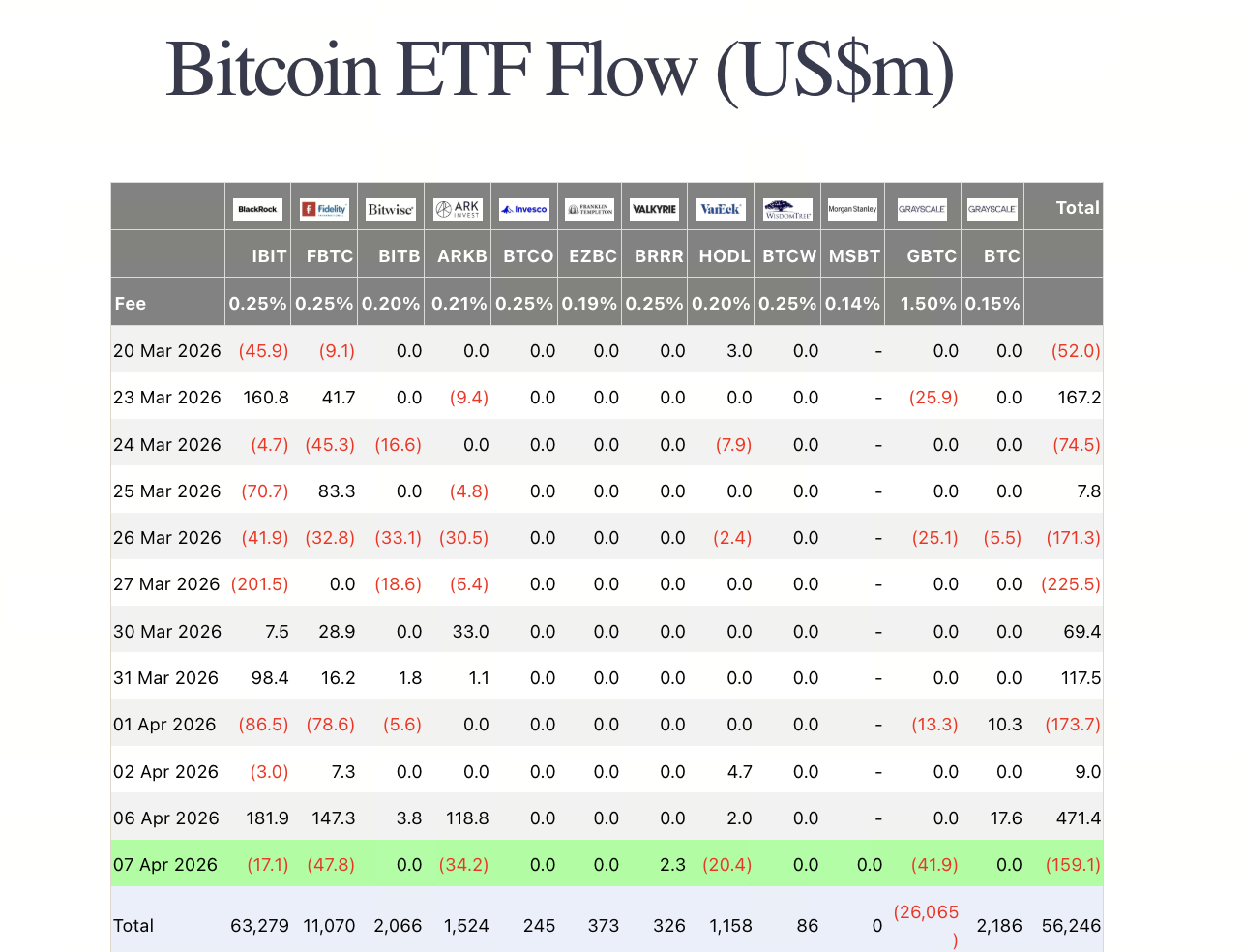

Image credit: Farside

Over the past year, Spot ETF capital flows have become the most quantifiable and widely discussed institutional capital metric in the crypto market.

This is no coincidence. ETFs offer three distinct advantages:

-

Transparent data: Daily net inflows, net outflows, and AUM are quickly available, allowing the market to track them in real time.

-

Simple, direct narrative: “Institutions are buying Bitcoin through ETFs” is far easier to grasp than explaining complex on-chain capital flows.

-

Clear price linkage: When ETFs see sustained net inflows, the market quickly links “institutional allocation increases” with “price appreciation.”

After March 2026, ETF inflows have indeed rebounded. Multiple market trackers show that US Spot Bitcoin ETFs recorded net monthly inflows in March 2026, ending several months of prior pressure. However, if you view ETFs as the entirety of institutional bids, the conclusion is overly simplistic.

ETFs are best seen as the “most visible entry point” for institutional capital, not the “sole carrier layer” for institutional demand.

Beyond ETFs: What Institutional Capital Is Entering the Crypto Market

Recent industry research and public cases show that, beyond ETFs, at least four types of capital are continuously impacting the crypto market.

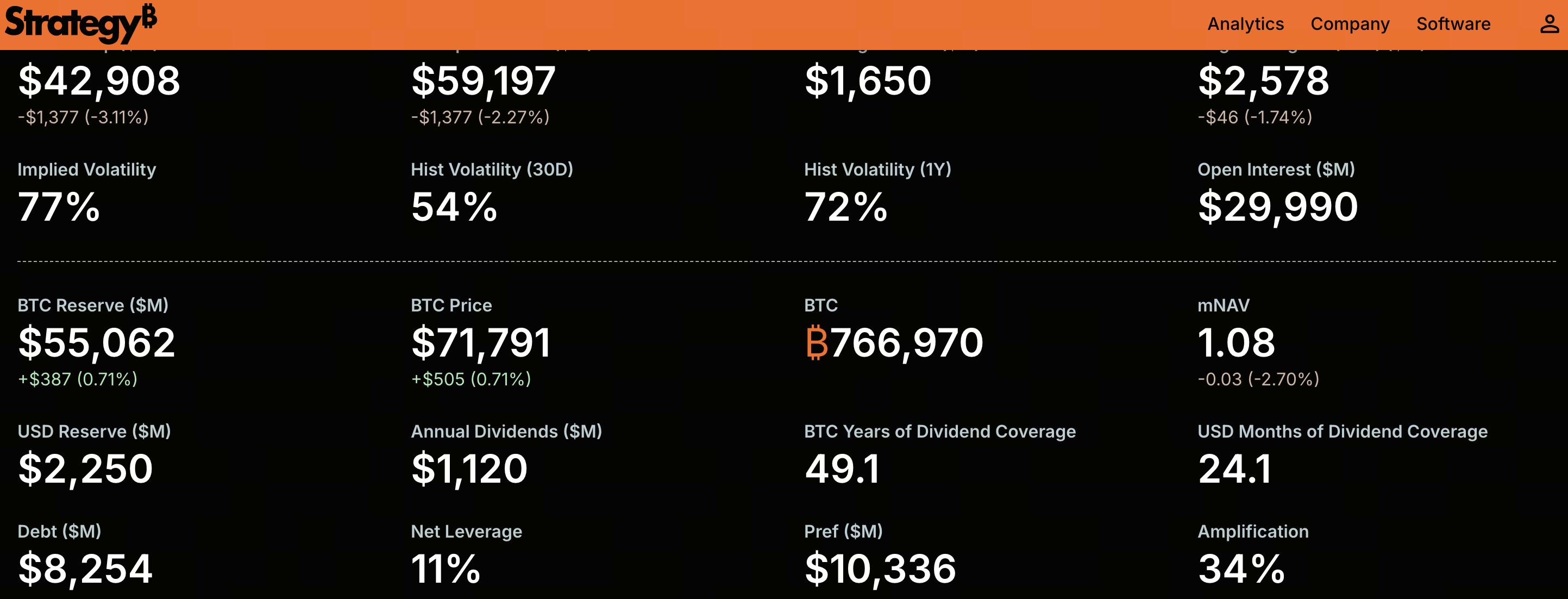

1. Digital Asset Treasury Companies

Image credit: Strategy official site

This is one of the most notable new variables of the past year. The 2026 Institutional Crypto Outlook notes that digital asset treasury companies have become an alternative allocation path alongside ETFs, with related firms raising a cumulative $29 billion to deploy crypto asset positions on their balance sheets.

These companies operate differently from traditional ETFs. Instead of passively holding assets for investors, they incorporate crypto assets into their capital structure and equity narrative. In effect, “holding crypto assets” becomes a core strategic component.

Their impact is mainly reflected in:

-

Bids may be more concentrated and event-driven

-

Capital sources extend beyond the secondary market, including additional issuance, convertible bonds, or private placements

-

Investors are not buying tokens directly, but gaining “crypto asset exposure with capital market premium”

2. Public Company Balance Sheet Allocations

While not new, this trend has gained traction since 2025. In May 2025, AP reported that Trump Media planned to build a $2.5 billion Bitcoin reserve through institutional share subscriptions and convertible bond financing. The spread of similar cases shows that crypto assets are no longer just the domain of tech or crypto-native firms—they are entering the capital operations of a broader range of public companies.

How do these bids differ from ETFs?

-

Allocation decisions are more influenced by corporate governance, financing conditions, and stock performance

-

Holding periods are typically longer, but entry points are more discrete

-

These actions are both asset allocation and, potentially, capital markets marketing strategies

In short, public company bids are not necessarily more “stable,” but they meaningfully reshape expectations for long-term demand.

3. Private Funds and Structured Investment Vehicles

Beyond visible ETFs and public companies, a significant portion of institutional capital enters the crypto market via private funds, closed-end vehicles, OTC structured products, and similar channels.

This capital is less transparent but more flexible, often excelling at tactical allocation, cross-market arbitrage, and volatility trading.

Compared to ETFs, this capital typically:

-

Is more sensitive to liquidity and exit options

-

Seeks yield enhancement, not just passive holding

-

Amplifies price elasticity during market volatility

As a result, their market impact is not a “slow variable,” but more of a periodic shock.

4. Quasi-Institutional Capital Behind Stablecoins and On-Chain Yield Products

This category is often the most overlooked.

From a market structure perspective, stablecoins, on-chain government bonds, on-chain cash management tools, and low-risk yield products are drawing increasing institutional capital into crypto infrastructure.

This capital may not directly “buy crypto,” but it influences the market by:

-

Providing dollar liquidity for on-chain trading

-

Lowering entry barriers for institutions moving into crypto

-

Serving as a parking pool for subsequent allocations to Spot, Derivatives, and RWA

In other words, these flows may not be the most visible, but they are likely the most critical “reserve layer.”

How Do New Institutional Bids Differ from ETFs

If ETFs represent a standardized, transparent, low-friction allocation path, new bids beyond ETFs form a layered structure.

Key differences include:

-

Holding objectives: ETFs focus on asset allocation and portfolio expression; treasury and public company allocations often involve equity narratives, financing strategies, and capital market premium logic.

-

Capital duration: ETF funds may appear “long-term,” but can be influenced by macro sentiment, interest rate expectations, and short-term risk appetite. Corporate allocations, once on the balance sheet, may exit even more slowly.

-

Trading behavior: ETF trades are typically transparent and timely; corporate treasury and private capital may concentrate purchases, delay disclosures, or use various hedging tools.

-

Market volatility impact: ETFs act as “directional confirmers,” while corporate treasury, structured capital, and on-chain dollar liquidity serve as “market elasticity amplifiers” or “underlying support layers.”

This means that future crypto market price movements cannot be explained by “ETF inflows” alone. Instead, it’s about who is buying, why, for how long, and through which instruments.

How Will Diversified Institutional Capital Change Market Structure

As institutional bids evolve from a single ETF narrative to a multi-layered structure, the market will see at least three changes:

1. Pricing Logic Will Become More Complex

Historically, ETF flows were the core directional indicator. But as treasury companies, corporate balance sheet allocations, and on-chain dollar systems expand, price drivers become more dispersed. Some rallies may result from corporate financing, equity revaluation, or on-chain liquidity expansion—not just traditional investment demand.

2. Market Volatility May Become More Structural

Many equate institutionalization with “greater market stability.” That’s not always the case. If new institutional capital sources come with leverage, financing constraints, or capital market narrative pressure, they may reinforce uptrends and amplify volatility during drawdowns.

3. Capital Style Will Shift from Passive Holding to Multi-Layered Strategy

Future institutional players may not simply allocate to spot, but will also engage in:

-

Spot and ETF allocation

-

Corporate equity and crypto asset-linked trading

-

Stablecoin and on-chain yield management

-

Derivative hedging and cross-market arbitrage

This evolution means the crypto market will increasingly resemble a multi-layered capital market, not just a one-way risk asset pool.

Risks and Common Misjudgments

When discussing “new institutional bids beyond ETFs,” it’s important to avoid several common misconceptions:

-

Assuming all corporate bids reflect long-term conviction: Some companies buy crypto for long-term allocation, others for capital market narrative. Don’t conflate the two.

-

Equating stablecoin growth with inevitable price appreciation: While stablecoin expansion boosts dollar liquidity, it doesn’t automatically translate into sustained net buying of spot assets.

-

Equating institutionalization with low volatility: Institutional entry increases market depth, but also adds leverage and trading complexity.

-

Treating public data as the whole story: ETF data is the most transparent, but transparency does not equal importance. Much of the capital truly moving the market doesn’t show up in ETF flow data immediately.

Conclusion: Institutional Bids Are Moving from a Single Entry Point to a Multi-Layered Structure

Beyond ETFs, who is reshaping the structure of institutional bids in the crypto market? Digital asset treasury companies, public companies integrating crypto assets into their balance sheets, private and structured vehicles, and quasi-institutional capital around stablecoins and on-chain yield products are together building a new bid system beyond ETFs.

This does not diminish the importance of ETFs. On the contrary, ETFs remain one of the clearest, most central, and most easily validated institutional entry points. But in 2026, focusing solely on ETF flows risks missing deeper structural changes.

What matters most is not just “are institutions buying,” but:

-

Through which channels are institutions entering

-

How long do they hold their positions

-

How do they impact market liquidity and volatility

In this context, crypto market institutionalization has entered a new phase. The market is moving beyond the single narrative that “only ETFs count as institutional bids” toward a more complex and mature capital structure.

Related Articles

Rising Prices but Bearish Funding Rates: Is Crypto Entering a “Layered Bull Market” After Wall Street Capital Inflows?

Fractional NFTs: Lowering Barriers and Enhancing Liquidity

USDD vs USDT: A Comparison of Stablecoin Mechanisms, Risks, and Use Cases

BlockDAG (BDAG): A High-Speed and Secure Layer 1 for the Next Era

Culper Research Shorts ETH: Fusaka Upgrade Controversy and the Structural Challenges of Ethereum’s Tokenomics